Some homeowners in Monmouth and Ocean counties who live in the state’s most flood-prone areas could face soaring insurance premiums under an ongoing overhaul of the federal flood insurance system, opens in a new windowaccording to new data released Monday by First Street Foundation.

The Brooklyn-based group looked at flood-prone areas throughout the nation to determine how much homeowners in those locations would have to pay if premiums reflected the actual annual risk of damage from flooding. The foundation looked at flood insurance rates and risk for single-family homes and other small multi-unit dwellings, like duplexes and triplexes.

It’s the first attempt to quantify the difference between the dollar amount of flood insurance policies and the amount of potential damage those policies would really cover, the foundation says.

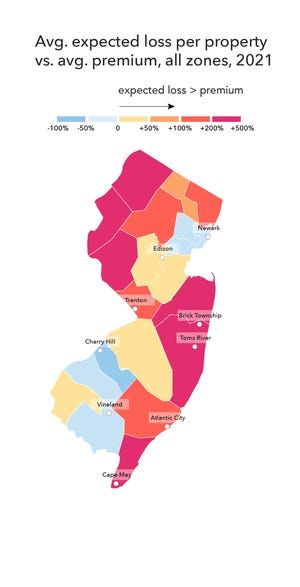

First Street’s calculations show that 27,005 Ocean County homes that the foundation suggests are most at risk are paying average annual premiums of $2,157, a number that should rise to $7,433 a year to accurately reflect the real risk of damage to the structures today.

That’s a 245% increase.

In Monmouth County, the 9,496 homes considered most flood-prone by First Street’s calculations pay annual average premiums of $1,826, which should rise to $6,145 to accurately reflect the real risk of damage.

The increase: 237%.

Nationwide, First Street found nearly 4.3 million homes across the country that have substantial risk of flood loss; flood insurance premiums would have to increase 4.5 times st to cover today’s risk.

The National Flood Insurance Program’s Risk Rating 2.0 is expected to use a similar model to determine new insurance rates, which are slated to go into effect Oct. 1.

It’s the most substantial change to the way flood insurance rates are set in more than 50 years, and it’s caused trepidation among both advocates and homeowners at the Jersey Shore. Until now, flood insurance rates have been determined by maps FEMA creates to predict which homes have a 1% annual risk of flooding.

Rates were determined by pooling the risk of groups of properties in designated flood zones; that means the owner of a $100,000 home would pay the same rate as the owner of a $1,000,000 home with the same flood risks, even though replacement costs are much higher for the more expensive house.

Under FEMA’s new formula, each home will receive an individual rating.

opens in a new windowFirst Street says its analysis is intended to help homeowners become more aware of the actual flood risk — and the financial consequences — as climate change leads to rising seas and more severe weather events.

Homeowners — and prospective buyers — can look up the flood risk and potential financial impact to individual properties at opens in a new windowhttps://floodfactor.com.

“Quantifying flood risk in concrete dollar terms creates a new context for homeowners to understand their risk, and for buyers to consider when evaluating a property,” said Matthew Eby, founder and Executive Director of First Street Foundation. “Flood risk brings with it real and potentially devastating financial impacts that aren’t being priced into the market or considered by most Americans.”

FEMA said that First Street’s estimates are just that – estimates.

“Any entity claiming that they can provide insight or comparison to the Risk Rating 2.0 initiative, including premium amounts, is misinformed and setting public expectations that are not based in fact,” said David Maurstad, senior executive for FEMA’s National Flood Insurance Program. “While entities are free to suggest or estimate their opinion of what flood insurance premiums should be, they are offering exactly that – an opinion – and they do not have insight into the Risk Rating 2.0 initiative.”

Some Shore residents and public officials have complained in recent years that FEMA’s flood maps have not taken into account the extensive mitigation efforts that have taken place since Sandy, while others believe flood maps aren’t taking into account potential increases in flooding as sea level rises.

Advocates say that increasing flood insurance rates without providing funds to help homeowners elevate their homes or pay for other mitigation efforts will not help reduce the risk of higher financial losses from storms.

“Currently, we’re approaching this about the dumbest way we could, and there are two ways we’re doing that,” said Amanda Devecka-Rinear, director of the New Jersey Organizing Project, an advocacy group. “First, we note flood risk is increasing and in some places maybe it’s been historically undercounted. FEMA’s approach right now is to say, ‘huh, more people are at risk, how can we charge them more money to reflect that risk?’ Should we instead be asking: what will it take to significantly mitigate the risks families face from flooding?

“Because that’s the second thing — what evidence do we have that charging people more will make us safer?” she said. ” What rising prices will mean without any significant investment in mitigation or affordability guarantees is simply that those who have will stay put, and those who have not will literally be washed away.”

Flood insurance premiums on primary homes could jump 5% to 18% per year when Risk Rating 2.0 comes into effect in October. Vacation homes could see flood insurance rise as much as 25% annually.

Homebuyers purchasing houses would have to pay the new rates immediately, a hefty increase in home costs that could hurt real estate markets in some waterfront areas.

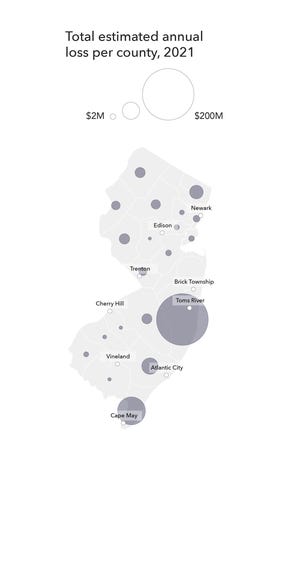

Toms River, which suffered more than $2 billion in property damage from superstorm Sandy, has 4,460 homes that are at extreme risk of structural damage from flooding. That’s the highest in the state, according to the foundation.

The township has the greatest projected flooding loss in the state this year, at nearly $41 million; that number is expected to grow to almost $57 million in 2051. Stafford’s Beach Haven West section is second, with about $21 million; First Street says that will grow to about $37 million in 30 years.

The owners of those homes are paying an average of $2,082 in flood insurance premiums; First Street says they should be paying $9,093 a year for flood insurance, or 337% more.

New Jersey has 46,963 properties that First Street considers to have extreme risk — in some cases these homes have had multiple flooding incidents. Those properties should be paying an average of $6,139 more a year to cover expected flood losses, according to the foundation’s data.

“They are going to basically just throw away everything they have done with mapping,” said George Kasimos, founder of the flood insurance advocacy group, Stop FEMA Now. He likened the coming change in flood insurance rates as similar to the way health insurance rates are set.

“They are going to do what’s done in healthcare; if you are old, if you’re overweight, you are going to pay more,” Kasimos said. “Now, if you are the first lagoon in from Barnegat Bay, the second lagoon, the eighth lagoon, the ninth lagoon, you are all paying the same rate. Each individual home is going to be rated now; people as you get closer (to the bay or ocean) are going to see severe increases.”

FEMA’s maps have previously been used to determine which homes must obtain flood insurance, and are relied upon when towns, states and counties are crafting their master plans for development. Flood insurance rates were set according to a home’s location within — or outside — of a flood zone, along with the structure’s elevation.

Homeowners outside the mapped areas are not required to buy flood insurance, but have been able to purchase policies at a discount to provide added protection for their properties.

But Risk Rating 2.0 will no longer rely on flood maps to determine premiums, and instead will look at the characteristics of individual houses: including foundation type, distance from water, and the replacement value of the home, according to a opens in a new windowJanuary report on the changes by the Congressional Research Service.

About 236,000 New Jersey property owners have flood insurance, and they pay an average premium of about $1,000. That number can soar into the thousands for properties FEMA considers more vulnerable.

Traditional homeowners insurance does not cover flood damage.

Increased NFIP premiums are a reckoning long overdue, said Carolyn Kousky, executive director of the University of Pennsylvania’s Wharton Risk Center and a First Street advisory board member.

Kousky said inaccurate pricing has left the NFIP in the red. But the new way FEMA will determine rates concerns many Jersey Shore homeowners who remember the aftermath of superstorm Sandy.

A FEMA review of the flood claims process found evidence of a potentially widespread scheme to fundamentally change the engineering reports that insurance companies rely on to determine if a structural damage claim is paid out, leading to underpayments on many flood claims.

New flood insurance rates under Risk Rating 2.0 were initially slated to go into effect October 2020, but the program was delayed for a year.

U.S. Sen. Robert Menendez, D-New Jersey, who lobbied for a delay in implementation of the new rates has been working for several years on a flood insurance reform bill that would cap premium increases at 9% a year, to protect. homeowners from huge cost spikes. Menendez’ reform bill also includes $1 billion for mitigation that homeowners could access before a storm floods their home.

Proactively investing in mitigation would do more to prevent future damage to homes than soaring flood insurance rates.

Jean Mikle covers Toms River and several other Ocean County towns, and has been writing about local government and politics at the Jersey Shore for nearly 36 years. A finalist for the 2010 Pulitzer Prize in public service, she’s also passionate about the Shore’s storied music scene. Contact her: @jeanmikle, 732-643-4050, [email protected].

Saving the Shore: opens in a new windowDoes Port Monmouth hold the answer to saving the Shore from sea level rise?

More: opens in a new windowHigh tide brings more flooding in Manasquan

Dune damage: opens in a new windowBay Head seeks emergency NJ permit to fix storm-battered dunes

Pingback: Climate displacement | SAVE THE STARLING